Africa’s banking sector is often celebrated for its resilience, innovation, and rapid digital growth. From mobile money breakthroughs to the rise of fintech ecosystems, the continent has become a global case study in leapfrogging traditional financial models. Yet beneath this progress lies a less visible reality, structural weaknesses that quietly limit the full potential of the industry. These weaknesses are what can be described as the “silent cracks” of African banking. They are not always obvious, and they do not always trigger immediate crises. Instead, they operate subtly, slowing down efficiency, increasing systemic risk, and widening the gap between financial institutions and the people they are meant to serve.

Some of these cracks include outdated legacy systems, fragmented regulatory frameworks, limited access to credit, trust deficits among customers, and inefficiencies in operational processes. Left unaddressed, they can hinder financial inclusion, reduce profitability, and weaken the long-term sustainability of banking institutions across the continent.

However, the story does not end with these challenges. Each crack also represents an opportunity for transformation. With the right mix of technology, policy reform, and innovative thinking, African banks can not only repair these weaknesses but turn them into strengths.

This discussion explores these silent cracks in detail, unpacking their root causes, their impact on the financial ecosystem, and most importantly, practical pathways to fixing them in a way that drives inclusive and sustainable growth.

The Friction Loop Problem

One of the most damaging yet often overlooked challenges in African banking is what can be described as the Friction Loop Problem, a self-reinforcing cycle where small operational failures gradually build into significant trust issues.

At first glance, these issues may seem minor like delayed transfer that takes hours instead of minutes, an ATM that debits an account without dispensing cash, a mobile app that crashes during peak usage and a failed transaction that takes days to reverse. Individually, these are operational hiccups. But collectively, and repeatedly, they create a loop of friction that steadily erodes customer confidence in the system. Read more on “Why Many African Youths Still Avoid Fintech and Digital Banking” to understand better

How the Friction Loop Works

The friction loop is not just about technical failure, it is about how those failures are handled. One of the ways a friction loop works starts with the initial disruption, where a customer encounters a failed or delayed transaction. Then the manual resolution bottleneck where the issue enters a manual review queue and often requiring human intervention, paperwork, or branch visits. Then there is a delayed feedback that the customer receives little or no real-time communication about what is happening.

Also, there is also a growing frustration where without clarity or speed, the customer’s trust begins to decline. The behavioral shift is also a problem because customer reduces usage, seeks alternatives (like fintech platforms), or loses confidence in formal banking. Check out “Reasons Why Fintechs Are Beating Traditional Banks”

Repetition or reoccurrence of issues is another huge issue on how friction loop works. When the same issues occur again, the frustration compounds faster. Over time, this loop becomes deeply embedded, turning small inefficiencies into systemic trust erosion.

Why It Matters More in Africa

In many African markets, where financial inclusion is still evolving, trust is everything. For many users, a single negative experience, especially involving lost or delayed funds, can push them back into informal financial systems. The consequences include:

- Reduced adoption of digital banking channels

- Increased reliance on cash and informal networks

- Slower growth for banks despite digital investments

- Competitive advantage shifting to fintechs that offer smoother experiences

Friction doesn’t just inconvenience customers, it drives them away.

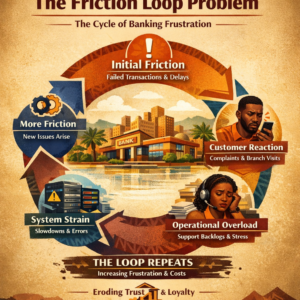

A Simple Diagrammatic Explanation Of Friction Loop Cycle

The diagram below clearly illustrates how the friction loop works.

┌───────────────────────────┐

│ Initial Friction │

│ (Failed transactions, delays,

│ system errors) │

└─────────────┬─────────────

▼

┌───────────────────────────┐

│ Customer Reaction │

│ (Complaints, retries, │

│ branch visits) │

└─────────────┬─────────────┘

│

▼

┌───────────────────────────┐

│ Operational Overload │

│ (Support pressure, │

│ manual work, backlog) │

└─────────────┬─────────────┘

│

▼

┌───────────────────────────┐

│ System Strain │

│ (Delays increase, │

│ errors rise) │

└─────────────┬─────────────┘

│

▼

┌───────────────────────────┐

│ More Friction │

│ (New failures, new issues) │

└─────────────┬─────────────┘

│

└───────────────► LOOP REPEATS

Breaking the Loop – Smart Autonomous Resolution Systems

To fix the friction loop, banks must move from reactive problem-solving to proactive system design. This is where automation and intelligent systems come in. A modern solution involves building a self-correcting banking system with three key capabilities:

1. Auto‑Reversal Checks – Instead of waiting for customers to report failed transactions, systems should automatically detect anomalies. For example, if a debit occurs without a corresponding successful transaction confirmation, ATM withdrawal fails but an account is debited and if a transfer stalls beyond a defined time threshold. The system should immediately flag the issue and trigger an auto-reversal process without human intervention.

The impact of this is the faster resolution (seconds or minutes instead of days), reduced operational workload and increased customer confidence.

2. Independence from Manual Review Queues -Traditional banking systems rely heavily on ticketing systems and escalation chains. These systems are slow, inconsistent, and prone to backlog. The smarter approach is to design rule-based and AI-assisted workflows that resolve common issues automatically, escalate only complex or high-risk cases and continuously learn from past incidents. This eliminates unnecessary dependency on branch visits, customer service calls and manual reconciliation teams.

The Impact of these includes scalable operations, consistent service delivery and significant cost reduction.

3. Real-Time Customer Updates – One of the biggest drivers of frustration is silence. Customers are more patient when they are informed. Banks should implement:

- Instant push notifications

- Transaction status updates

- Clear timelines for resolution

- Confirmation alerts once issues are resolved

Imagine receiving a message like: “We noticed a failed transaction on your account. A reversal has been initiated and will reflect within 2 minutes.” This level of transparency transforms the experience entirely.

The resultant factor in this will be a reduced anxiety and uncertainty, stronger trust in the system and improved customer satisfaction.

How Smart Banks Break the Friction Loop

1. Stop Friction at the Source – Banks should improve transaction processing reliability, monitor failures in real time and fix root causes, not symptoms.

2. Reduce Customer Effort – There should be a clear transaction feedback (success/failure instantly), reduce repeated steps and simplify digital journeys.

3. Speed Up Resolution – Banks and other institutions should increase resolution timeline with fast reversal systems, automation of dispute handling and empower frontline staff with faster tools.

4. Design for Load, Not Just Speed – Banks must anticipate high transaction volume, peak-time failures and customer behavior during outages

5. Use Data to Detect Friction Early – In the tracking of failed transactions, complaint patterns and drop-off points in digital channels, banks should use data to detect frictions early.

Here is The Bigger Picture – From Friction to Flow

Solving the friction loop is not just about fixing errors, it’s about redefining how banking systems interact with customers. When banks detect issues instantly, resolve them autonomously and communicate proactively, they shift from a model of friction to one of flow. In such a system, failures will still happen (as they always will in any complex system) but customers barely feel them and trust is preserved and even strengthened.

The Final Insight

The real danger of the friction loop is not the errors themselves, it is the compounding effect of unresolved experiences. African banking does not need to eliminate every failure. That is unrealistic. What it must do is eliminate the friction around failure. By embedding automation, intelligence, and transparency into operational processes, banks can break the loop and in doing so, turn one of their biggest weaknesses into a defining competitive advantage.

Leave a Reply